News Asia

Hitachi Launches Sustainable HVAC Solutions for Southeast Asia’s Growing Data Centre Sector

Southeast Asia’s rapidly expanding data centre industry is driving demand for advanced cooling technologies, and Hitachi Cooling & Heating is positioning itself at the forefront of this shift. The company has recently launched a new range of energy-efficient HVAC and chiller systems designed specifically for the region’s tropical climate and rising digital infrastructure needs.

As countries such as Singapore, Malaysia, Indonesia, and Thailand become key data centre hubs, the strain on electricity and water resources has intensified. Cooling systems account for a significant portion of data centre energy consumption, making efficiency a critical concern. Hitachi’s newly introduced S Series, VG Series, and VM Series chillers aim to address this challenge by reducing energy use while maintaining high reliability under heavy workloads.

A key feature of these systems is their use of low global-warming-potential (GWP) refrigerants, helping operators meet increasingly strict environmental regulations. The chillers are also designed to perform efficiently in high-humidity and high-temperature environments, which are common across Southeast Asia. This makes them particularly suitable for urban data centres where space, power availability, and water use are tightly constrained.

Beyond environmental benefits, the new HVAC solutions support long-term cost savings for operators by lowering operational expenses and improving system lifespan. With governments across the region pushing for greener infrastructure and carbon-reduction targets, such technologies are becoming essential rather than optional.

As Southeast Asia continues to attract investment in cloud computing, artificial intelligence, and digital services, sustainable HVAC systems like these are expected to play a central role in enabling data centre growth without overwhelming local power grids or water supplies.

Climate Change Increasingly Threatens Asia’s Power and Water Infrastructure

Across Asia, climate change is placing growing pressure on critical power and water infrastructure, raising concerns about long-term resilience and service reliability. Recent assessments warn that extreme heat, floods, and prolonged droughts are disrupting electricity generation, water supply systems, and sanitation networks in several countries, including India, Indonesia, Malaysia, and China.

Rising temperatures have reduced the efficiency of thermal power plants, while erratic rainfall has impacted hydropower generation by lowering river flows. At the same time, severe flooding has damaged substations, pipelines, and water treatment facilities, resulting in costly repairs and service interruptions. These climate-related disruptions are becoming more frequent, increasing operational risks for utilities across the region.

Experts warn that Asia’s fast-growing cities are particularly vulnerable. Aging infrastructure, rapid urbanization, and inadequate climate adaptation planning have left many systems ill-prepared for extreme weather. In coastal and low-lying areas, saltwater intrusion is contaminating freshwater sources, further complicating water management efforts.

According to regional development institutions, Asia will require trillions of dollars in investment over the coming decades to climate-proof its power and water systems. This includes upgrading transmission networks, diversifying energy sources, strengthening flood defenses, and improving water efficiency through smart monitoring technologies.

Governments and utilities are increasingly exploring nature-based solutions, renewable energy integration, and digital infrastructure to improve resilience. However, experts stress that without coordinated policy action and sustained investment, climate change could significantly undermine economic growth, public health, and energy security across the continent.

AIIB Mobilizes $6 Billion to Accelerate Sustainable Infrastructure Across ASEAN

The Asian Infrastructure Investment Bank (AIIB) has announced a major financing initiative aimed at boosting sustainable infrastructure development across the ASEAN region. Partnering with leading financial institutions including Maybank, CIMB, AmBank, and BPMB, the bank plans to mobilize up to USD 6 billion for projects focused on clean energy, water systems, and climate-resilient infrastructure.

The funding will support a wide range of sectors, including renewable power generation, smart utilities, water treatment, and low-carbon transport. These investments are designed to help fast-growing Southeast Asian economies meet rising infrastructure demands while aligning with global climate goals.

Urbanization and population growth across ASEAN have placed significant pressure on existing infrastructure, particularly in energy and water supply. Many cities are struggling to expand services without increasing carbon emissions or environmental degradation. AIIB’s initiative aims to bridge this gap by promoting private-sector participation and innovative financing models.

By working with regional banks, the program also seeks to improve access to long-term capital for infrastructure developers and utilities. This approach is expected to accelerate project implementation while strengthening financial resilience in local markets.

AIIB officials emphasized that sustainable infrastructure is critical for long-term economic stability in Asia. Investments in resilient power grids, efficient water systems, and clean energy not only reduce climate risks but also support job creation and regional competitiveness.

The initiative reflects a broader shift toward green finance in Asia, as governments and financial institutions increasingly prioritize infrastructure that can withstand climate shocks while supporting inclusive growth.

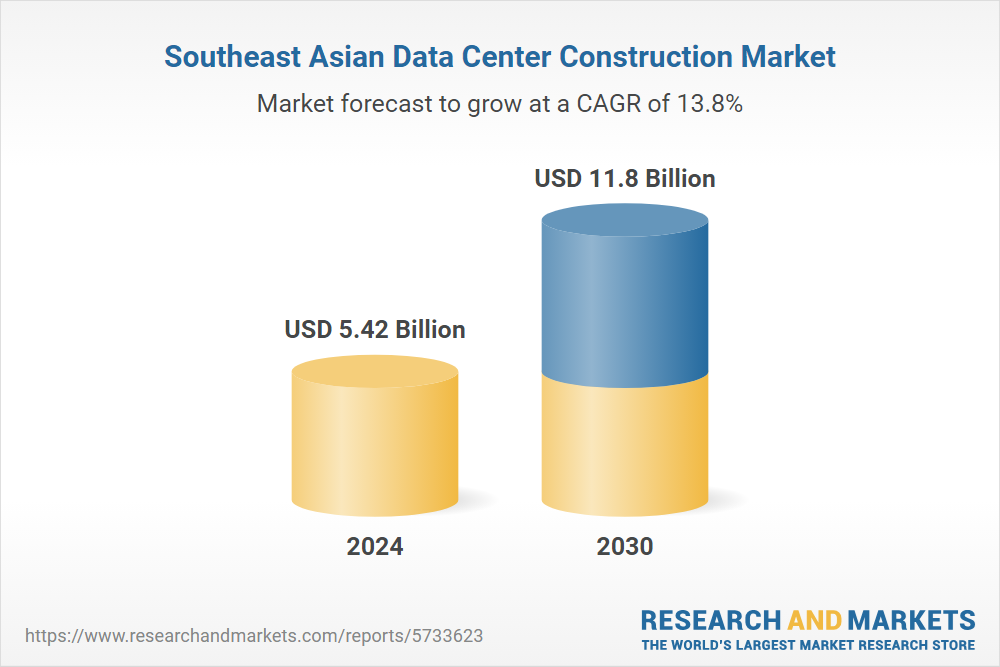

Data Centre Construction Boom in Asia Raises Power and Cooling Challenges

The Asia-Pacific region is experiencing a sharp surge in data centre construction, driven by rising demand for cloud services, artificial intelligence, and digital connectivity. Southeast Asian markets such as Singapore, Malaysia, Vietnam, and Indonesia are emerging as key destinations, but the rapid expansion is creating new challenges for power supply and HVAC infrastructure.

Industry reports indicate that the region’s data centre construction market is set to grow rapidly through the end of the decade. However, data centres are among the most energy-intensive facilities, placing heavy pressure on local electricity grids. In response, developers are increasingly adopting modular power systems, on-site energy storage, and renewable energy sourcing to reduce grid dependency.

Cooling remains one of the biggest challenges, particularly in tropical climates. Operators are turning to advanced HVAC solutions, including liquid cooling, high-efficiency chillers, and AI-driven thermal management systems to control energy use and maintain operational reliability.

Governments across the region are responding with supportive policies, such as tax incentives, streamlined approvals, and renewable energy mandates for large data facilities. These measures aim to balance digital infrastructure growth with sustainability and grid stability.

Experts warn that without careful planning, uncontrolled data centre expansion could strain power and water resources. As a result, future projects are increasingly designed with energy efficiency, heat reuse, and water conservation in mind, signaling a more sustainable approach to digital infrastructure development in Asia.

Japan’s Earthquake-resilient real estate

One of the foundations of Japan’s success in earthquake safety is its strict and continually updated building code. Since significant revisions in the late 20th century, especially post-1981, the standards require engineers to design buildings that not only resist collapse but also protect occupants during strong earthquakes. Moderncodes account for soil type, foundation depth, height, and added shock-absorbing technologies.

Buildings undergo mandatory inspections during construction and after major seismic events, ensuring long-term resilience.

Innovative engineering also plays a major role. Many structures use seismic isolation bearings, allowing the building to move with quake forces rather than fight them. Advanced damping systems, such as oil or pendulum dampers, absorb and dissipate energy, significantly reducing building sway. New materials like flexible exterior coatings further prevent cracking and falling debris, enhancing safety for residents and pedestrians.

Beyond safety, earthquake resistance is becoming a financial advantage. Properties built or retrofitted to modern seismic standards often command higher market value and attract better insurance terms. In Japan, insurance premiums can be discounted for buildings with base isolation or high resistance classifications, making resilient buildings attractive investments. Government incentives, including tax breaks and subsidies for retrofitting older structures, further promote seismic upgrades.

As other earthquake-prone countries look to reduce risk and protect property value, Japan’s model shows how seismic engineering and stringent regulation can turn natural hazard mitigation into a real estate strength.

India Upgrades National Highway Corridor to Boost Connectivity and Safety

The Indian government has approved a major upgrade to a 100-km stretch of National Highway-16 (NH-16) between Muppavaram in Prakasam district and Kaja in Guntur district, converting it into a fully access-controlled corridor to enhance connectivity across Andhra Pradesh. This move is part of a broader push to modernize the country’s infrastructure network, aiming to facilitate faster travel between key economic hubs while improving road safety and regional trade flows.

The project will transform the existing six-lane highway into an access-controlled expressway, eliminating direct access from local roads and reducing conflict points that often lead to accidents. Instead, vehicles will use designated entry and exit points, which is expected to reduce congestion and ensure smoother traffic flow, especially for long-distance freight movement. Toll collection will be structured on a distance-based system, aligning with global best practices for toll financing.

Another key feature of the upgrade will be the construction of service roads on both sides of the highway, allowing local traffic to move safely without interfering with high-speed expressway operations. A Detailed Project Report (DPR) will be prepared within a year, detailing land acquisition requirements, environmental considerations, and cost estimates. The planning authority, under the Indian Ministry of Road Transport & Highways, has emphasized compliance with environmental safeguards and community impact mitigation. (The Times of India).

This infrastructure development aligns with India’s larger strategy to expand its expressway network under national initiatives to support economic growth. Expressways like this provide critical links between industrial zones, ports, and agricultural regions, supporting job creation and economic diversification. Analysts also note that better highways attract private investment and ease the logistics burden for exports, making India more competitive in global markets.

Pakistan and ADB Sign $730M Deals to Strengthen National Power Grid

In a move to reinforce Pakistan’s energy infrastructure, the Asian Development Bank (ADB) and the Government of Pakistan have signed two major financing agreements totaling $730 million, aimed at modernizing the country’s power transmission system and accelerating State-Owned Enterprise transformation.

Under the agreements finalized in late December 2025, $330 million has been allocated to the Second Power Transmission Strengthening Project, which seeks to upgrade and expand the national grid. The project is expected to enhance the system’s ability to evacuate electricity from

new and upcoming hydropower plants across the country — enabling more reliable energy distribution and reducing transmission bottlenecks that have historically hampered Pakistan’s electricity supply stability.

The remaining $400 million will fund the Accelerating SOE Transformation Program, a policy-focused initiative designed to improve the governance, transparency, and efficiency of Pakistan’s state-owned entities. Officials highlighted that this program aims to align the operational performance of key infrastructure agencies, such as the National Highway Authority and power utilities, with international best practices.

ADB Country Director Emma Fan noted that these agreements reflect the bank’s confidence in Pakistan’s reform efforts and its commitment to supporting sustainable infrastructure development. Strengthening the power grid is seen as critical for unlocking the potential of Pakistan’s hydropower resources, which, once fully tapped, could help reduce reliance on expensive fossil fuels and improve energy affordability for consumers.

Investors and policy analysts have also applauded the focus on institutional transformation, saying that stronger governance and financial discipline within infrastructure agencies will attract greater private investment and enhance public-sector project delivery.

Remote Indo-Nepal Border Village Sees Major Infrastructure and Water Improvements

In the remote village of Chaugurji, located along the India–Nepal border, longstanding infrastructure deficits are being addressed through a suite of recent government interventions that promise to transform local livelihoods. Residents who once endured hours-long journeys for basic services can now reach nearby towns in minutes thanks to the construction of a new pontoon bridge over the Karnali and Mohana rivers.

Alongside improved connectivity, the village has benefited from India’s Jal Jivan Mission, which has provided tap water connections to every household. This initiative eliminated dependence on arsenic-contaminated groundwater, significantly improving public health outcomes and offering safe water access for cooking, cleaning, and other daily needs.

Solar-powered street lighting has enhanced safety and community activity after dark, while digital inclusion projects — such as smart classrooms and solar-powered learning facilities in primary schools — are equipping children with modern educational tools and opportunities comparable to urban peers.

Local officials emphasize that these improvements are part of a broader strategy to reduce rural isolation and promote equitable development in border regions. By linking Chaugurji to essential services like healthcare, education, and markets, planners aim to foster economic activity and reduce migration pressures toward cities. Solar lighting and classroom technologies also underscore a shift toward sustainable, resilient community infrastructure in line with national goals.

Residents report that the changes have already boosted agricultural productivity, reduced school absenteeism, and improved emergency response times. As infrastructure projects continue, officials hope that Chaugurji’s transformation will serve as a model forsimilar rural communities across the region.

Nepal Strengthens Regional Energy Cooperation Through Historic Hydropower Trade

Nepal is increasingly emerging as a key player in South Asia’s clean energy landscape, highlighted by the recent launch of trilateral hydropower trade involving Nepal, India, and Bangladesh. This agreement marks the first of its kind in the region, enabling Nepal to export 40 megawatts of electricity to Bangladesh through India’s transmission grid, while collaboration on larger hydropower ventures continues to advance. The initiative is part of broader regional cooperation efforts designed to optimize South Asia’s renewable energy potential and address shared electricity shortages. Hydropower-rich Nepal has leveraged its abundant water resources to become an energy exporter, supplying clean electricity that complements India’s energy mix and supports Bangladesh’s growing demand.

Beyond electricity trade, India, Nepal, and Bangladesh are jointly developing the 683 MW Sunkoshi-3 hydropower project. Located approximately 60 km from Kathmandu, this project represents a significant investment in regional infrastructure and reflects strengthened diplomatic ties across borders. The collaborative model brings together government agencies and private developers from all three countries in a rare example of transnational energy integration.

Officials from Kathmandu have emphasized the economic and environmental benefits of expanding hydropower capacity, noting that clean energy exports will generate revenue, reduce fossil fuel imports, and help stabilize regional grids. For Bangladesh, the additional electricity supply provides much-needed capacity during peak demand periods, while India benefits from enhanced grid connectivity and export transit fees.

Energy analysts say that Nepal’s hydropower trade could serve as a blueprint for deeper South Asian cooperation on renewable infrastructure, potentially extending to other countries where shared water resources and grid systems can support sustainable power solutions.

Cambodia’s Funan Techo Canal Project Advances to Improve Waterway Trade

Cambodia is progressing on the ambitious Funan Techo Canal project, a 180 km waterway that aims to connect the Mekong River at Takeo with the Phnom Penh Autonomous Port and the Gulf of Thailand. The project, officially named the Tonle Bassac Navigation Road and Logistics System Project, is designed to boost inland water transport, reduce logistics costs, and catalyze economic growth across southern Cambodia.

Construction began with a groundbreaking ceremony in August 2024, and land demarcation and preparation for Phase I were reported to be over 50 percent complete by late 2024. Once finished — with a target date around 2028 — the canal will support vessels up to 3,000 DWT, opening a major commercial route from Cambodia’s interior to international shipping lanes.

The infrastructure plan includes building three dams with sluices and eleven bridges, along with widened navigation channels and modern port facilities. This combination of hydraulic and transport infrastructure is expected to improve water management, flood mitigation, and year-round navigability in regions prone to seasonal water fluctuations.

Funding for the US$1.7 billion project has involved both Cambodian and Chinese stakeholders, although investor confidence has fluctuated amid concerns about economic returns and long-term maintenance costs. The Cambodian government has nonetheless pushed ahead, seeking to develop a more resilient and diversified logistics network that reduces dependence on road transport and enhances trade competitiveness with neighboring countries.

Officials argue that once operational, the canal will not only strengthen Cambodia’s internal trade connectivity but also support regional integration by linking with broader Mekong basin transport initiatives — potentially benefiting Vietnam, Thailand, and beyond.

Hitachi Launches Advanced HVAC Chillers to Power Data Centre Growth in Southeast Asia

Hitachi Cooling & Heating has recently rolled out a new line of next-generation HVAC centrifugal chillers aimed at supporting the booming data centre sector in Southeast Asia. As the region continues to attract global investment in cloud computing, artificial intelligence, and digital infrastructure, efficient and sustainable cooling has become a critical operational priority. Traditional cooling systems account for a significant share of energy use in data centres, and energy costs can make or break long-term profitability for operators. To address this need, Hitachi’s S Series, VG Series, and VM Series chillers have been engineered to offer high reliability, rapid response after outages, and advanced energy management features — a strong value proposition for data centre developers and facility managers alike.

One of the standout technical features of the new chillers is their ability to restart within just 35 seconds after a power interruption. In environments where continuous cooling is essential to prevent overheating and equipment failure, this rapid restart capability can drastically reduce operational risk and downtime. Alongside this, the systems use Direct Drive Inverter Technology, which adjusts cooling output based on real-time load and environmental conditions, improving energy efficiency and lowering overall operational costs. These capabilities are especially relevant in Southeast Asia, where power constraints and rising electricity prices are key challenges for large facilities.

Environmental sustainability is another core focus. The chillers employ low global-warming-potential (GWP) refrigerants such as R513A, R1233zd, and R1234ze, supporting both corporate carbon-reduction goals and stricter regional regulatory standards on refrigerants. This aligns with broader industry efforts to reduce the carbon footprint of cooling systems, which are responsible for a significant share of energy use in buildings and industrial facilities.

With data centre infrastructure expanding rapidly across Singapore, Malaysia, Thailand, and Vietnam, cooling efficiency is becoming a decisive factor in site selection and design. Hitachi’s advanced chillers aim to set a new performance benchmark for sustainable HVAC solutions in the region’s competitive digital infrastructure landscape.