SPECIAL REPORT

2026 Global

Infrastructure

Investment Review

The Age of Pragmatic Green Growth

As we move through 2026, the global infrastructure investment landscape has entered what analysts are calling a “Supercycle of Execution.” After years of high-level net-zero pledges, the focus has shifted from ambitious rhetoric to the gritty, capital-intensive reality of building the physical backbone of a decarbonized economy. Global infrastructure needs are now projected to exceed $100 trillion by 2040, and 2026 stands as a pivotal year where the convergence of digitalization, decarbonization, and energy security is dictating capital flows.

While the “green” label remains a primary driver, the motivations have evolved. Green investment in 2026 is no longer just a matter of environmental stewardship; it is increasingly viewed through the lens of industrial competition, national security, and the insatiable power

demands of the Artificial Intelligence (AI) revolution.

1. The AI-Energy Nexus: A New

Infrastructure Driver

Perhaps the most significant shift in 2026 is the role of AI as a primary catalyst for green infrastructure. The global data center build-out has accelerated beyond early- decade projections, with investment in data infrastructure expected to reach $620 billion this year.

- Firm Clean Power: Hyperscalers (Amazon, Google, Microsoft) are no longer satisfied with “bundled” renewable credits; they are now direct investors in “firm” low-carbon power. This has led to a resurgence

in nuclear energy and a massive scale-up of Battery Energy Storage Systems (BESS).

- Grid Modernization: In 2026, the “grid bottleneck” has become the single largest risk to both digital and green transitions. Consequently, investment in power grids is surging, with global spend expected to approach $500 billion this year. The focus is on “smart

Grids” capable of bidirectional flow and the integration of decentralized energy resources.

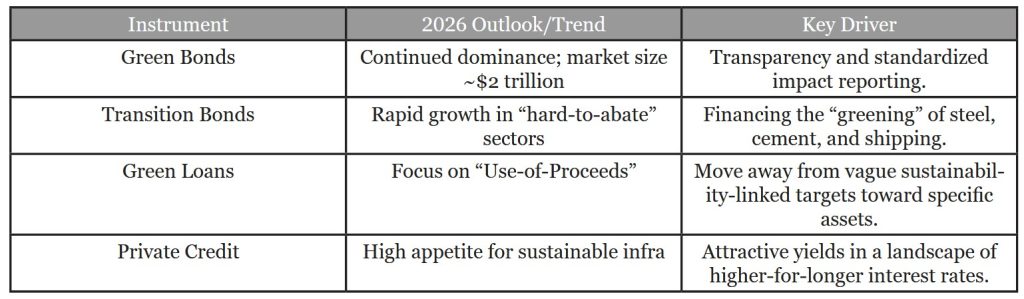

2. Green Finance: From Billions to Trillions

The financial instruments supporting these projects have matured significantly. Sustainable bond issuance is

expected to exceed $1 trillion in 2026, underpinned by a

more “steely pragmatism” among institutional investors.

3. Regional Shifts: The “Great Fragmentation”

The “one-size-fits-all” model of global green investment has given way to a fragmented, regionally distinct landscape shaped by industrial policy.

The United States: Despite some rollbacks of early-decade subsidies, the U.S. remains a powerhouse of “safe-harbor” projects. Developers are front-loading construction to secure tax eligibility, while the Foreign Entity of Concern (FEOC) rules are forcing a massive onshoring of the green supply chain—from lithium refining to solar cell manufacturing.

China: China remains the world’s largest renewable market, but its focus has shifted from sheer capacity to grid stability and export dominance. China now accounts for nearly 50% of the world’s offshore wind growth and leads globally in pumped-storage hydropower.

Europe: Faced with high energy costs, Europe is doubling down on “Strategic Autonomy.” The Carbon Border Adjustment Mechanism (CBAM) is now a major factor, forcing global exporters to certify the carbon footprint of the infrastructure used to produce their goods.

Emerging Markets: A widening gap persists. While India is becoming a “swing factor” for global climate goals with its massive solar auctions, many African nations struggle under high debt-servicing costs that equal nearly 85% of their total energy investment.

4. The Rise of “Resilience and Adaptation”

A major theme of 2026 is the mainstreaming of Adaptation Finance. With physical climate risks (wildfires, floods, extreme heat) now impacting municipal bond ratings and insurance premiums, investors are allocating more capital to “climate-proofing” existing infrastructure.

“In 2026, the economics of cleantech has overtaken the politics. We are no longer debating if we should build green, but how fast we can build it to ensure economic resilience.”

This shift is visible in the G7’s Partnership for Global Infrastructure and Investment (PGII), which aims to mobilize $600 billion by 2027. Much of this is targeted at “green corridors”—integrated transport and energy networks in Africa and Southeast Asia designed to secure supply chains for critical minerals like nickel and graphite.

5. Key Challenges and Risks

Despite the momentum, 2026 is not without its “growing pains”:

- Affordability & Regulatory Risk: As utilities pass the costs of massive grid upgrades to consumers, political backlash over rising electricity bills is a growing concern.

- Supply Chain Volatility: The move toward “de- risking” from Chinese components has increased the cost of wind and solar projects in the West by 30-50% in some regions.

- The “Show Me” Period for AI: There is mounting pressure on the tech sector to prove that the massive infrastructure investments are delivering the promised productivity gains.

Case Studies

Building on the global overview, the regional dynamics of 2026 reveal two distinct models of green infrastructure development: Europe’s transition from a “subsidy-led” to an “industry-first” powerhouse, and Southeast Asia’s shift from bilateral projects to a unified regional energy market.

Regional Deep Dive: The EU and Southeast Asia

1. The European Union: Transitioning to “Clean Industrialism”

In 2026, the European Union is navigating a critical fiscal crossroads. The NextGenerationEU recovery fund, which fueled the initial post-pandemic green surge, is nearing its expiration. In its place, the EU has pivoted toward the Clean Industrial Deal, prioritizing infrastructure that directly supports domestic manufacturing and energy sovereignty.

Key 2026 Focus Areas:

- The “Made in Europe” Procurement Shift: Starting this year, new EU rules favor green technologies manufactured within the bloc for public tenders. This is a direct response to global competition, ensuring that the €1.2 trillion annual investment required for net-zero goals also builds the European industrial base.

- The Hydrogen Backbone: 2026 marks the first year of large-scale construction for the European Hydrogen Backbone. Notable projects include the Gronau underground storage facility in Germany—the first of its kind to receive cross-border EU funding—designed to stabilize the industrial heartlands of Northwest Europe.

- Cross-Border Interconnectivity: The EU has allocated €650 million in new grants this year for 14 flagship energy projects. These focus on integrating the “energy islands” of the Baltics and improving the flow of cheap solar power from the Iberian Peninsula to the high-demand centers of Central Europe via projects like the Aguayo II pumped-storage plant in Spain.

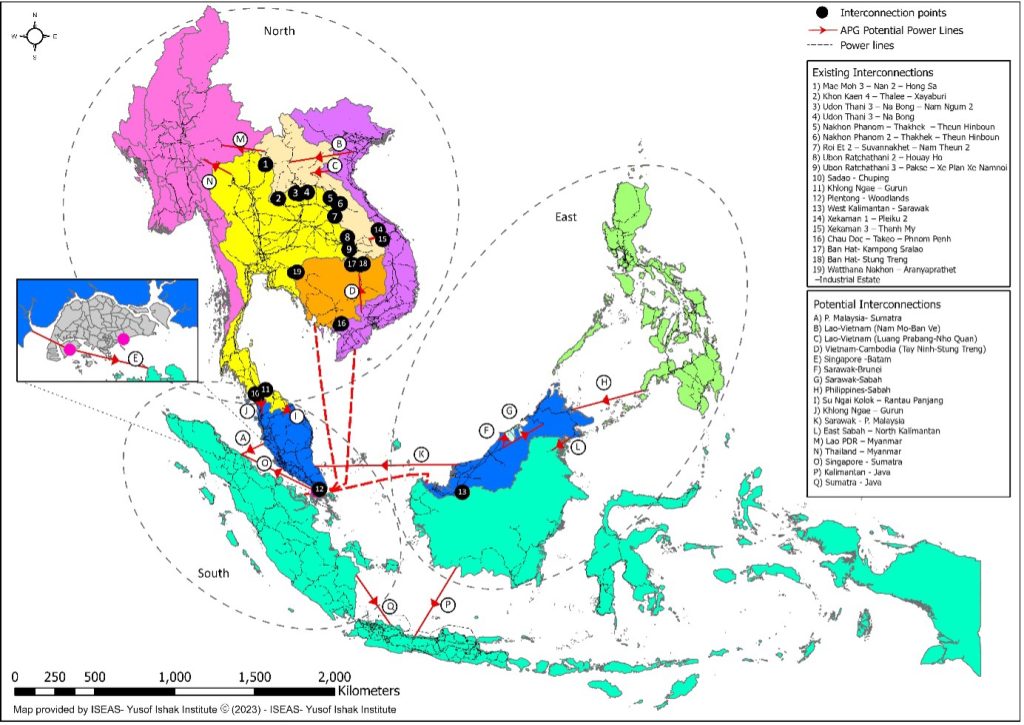

2. Southeast Asia: The Rise of the ASEAN Power Grid (APG)

In Southeast Asia, 2026 is being defined by the “connectivity leap.” Historically, the region relied on isolated national grids. This year, the implementation of the ASEAN Plan of Action for Energy Cooperation (APAEC) 2026–2030 has catalyzed a shift toward a multi-lateral energy market.

Key 2026 Focus Areas:

- The “Battery of Southeast Asia” Maturity: Laos has successfully expanded its hydropower export capacity, but the 2026 strategy has shifted focus toward green hydrogen. Leveraging seasonal hydro excesses, Laos is positioning itself to export carbon-neutral fuels to its neighbors.

- The Green Energy Auction Program (GEAP): The Philippines has emerged as a regional leader in private capital mobilization. By allowing 100% foreign ownership in renewable assets and conducting massive auctions (targeting 35% RE by 2030), it has become the most attractive “pure-play” renewable market in ASEAN this year.

- The Digitalized Grid: In Indonesia and Vietnam, the focus has moved to Smart Grid Control Centers. After the “solar boom” of the early 2020s strained Vietnam’s infrastructure, 2026 investments are dominated by grid-firming technologies and AI-driven load management to prevent curtailment.

Regional Fact: ASEAN requires roughly $200 billion per year in green investment through 2030. In 2026, for the first time, private credit and blended finance (via the ADB and World Bank) are providing over 70% of this capital, reducing the historical reliance on state-owned utility balance sheets.

3. Comparing the Two Landscapes

While both regions are scaling rapidly, their challenges in 2026 differ:

The EU is struggling with regulatory complexity and the transition from public subsidies to private market sustainability. Its main hurdle is “speed to market” for permitting.

Southeast Asia is battling institutional readiness. While the technology and capital are available, harmonizing grid codes and cross-border legal frameworks remains the primary “soft infrastructure” challenge of the year.

Summary: The 2026 Inflection Point

The narrative of 2026 is no longer about the necessity of green investment, but the efficiency of its execution. Whether it is the EU protecting its industrial core or ASEAN integrating its disparate markets, infrastructure has become the primary tool for securing economic relevance in a decarbonizing world.